Czech Crown Intervention and its Impact on EUR/CZK

Subscribe

Dear Traders,

The Czech National Bank (CNB) is expected to hold a Bank Board meeting today on Thursday 30 March 2017 where it discusses the monetary policy of the Czech Republic. This is expected to impact the CZK in general and the EUR/CZK in specific.

The board will review a situation report on the monetary and economic developments within the Czech nation. In the last 2 years since spring 2015, the CNB has made interventions to weaken the Czech Crown (CZK), the national currency, in an attempt to boost the economy and inflation to 2%. The monetary policy of CZK weakness seems to have been successful as the Czech economy is showing strong results:

- GDP growth of 1.7% in 4th quarter 2016

- Inflation hitting and rising above 2% (2.2% in Jan and 2.5% in Feb 2017)

- Only 3.4% unemployment – lowest level of unemployment in EU

- Public debt only 37.2% of GDP

- Yearly budget surplus of 61 billion CZK in 2016 (currently around 2.3 billion euro)

The CNB intervention to weaken the Crown has made exports cheaper, especially to Germany which is the primary trade partner of the Czech Republic.

The weakening of the CZK took the average EUR/CZK rate of 25 up to a stable 27 for the last few years.

Why the Czech intervention will soon stop

There are in fact a coupe strong arguments why the intervention of the Czech National Bank (CNB) in the Czech Crown (CZK) will soon stop:

- Because the Czech National Bank has announced that its intervention to weaken the CZK will be removed by the second quarter of 2017, or perhaps even earlier at the end of the first quarter 2017.

- Because the Czech economy is moving forward strongly and the monetary policy support is not needed anymore. In fact, the Czech Republic is exceeding its 2% inflation target and hence might even decide to raise the interest rate in the near future.

- Because the intervention is expensive. The CNB needs to sell Crowns and Buy Euros to keep the exchange rate at 27. The intervention in January and February of 2017 is apparently already exceeding the total intervention level of 2016. The level of speculation – domestic and international – could also be picking up as the traders and investors expect the CZK to strengthen by the end of the year and in the next few years.

The announcement of the monetary policy decision by the CNB will take place at 1pm local time (CEST time zone) on Thursday 30 March 2017. The press conference will be held at 2:15pm. The statement will show a list of risks to the current forecast, the Board’s decisions regarding interest rate including the ratio of the votes and a brief summary of the information used to make decisions. The minutes of the meeting are published 8 days later.

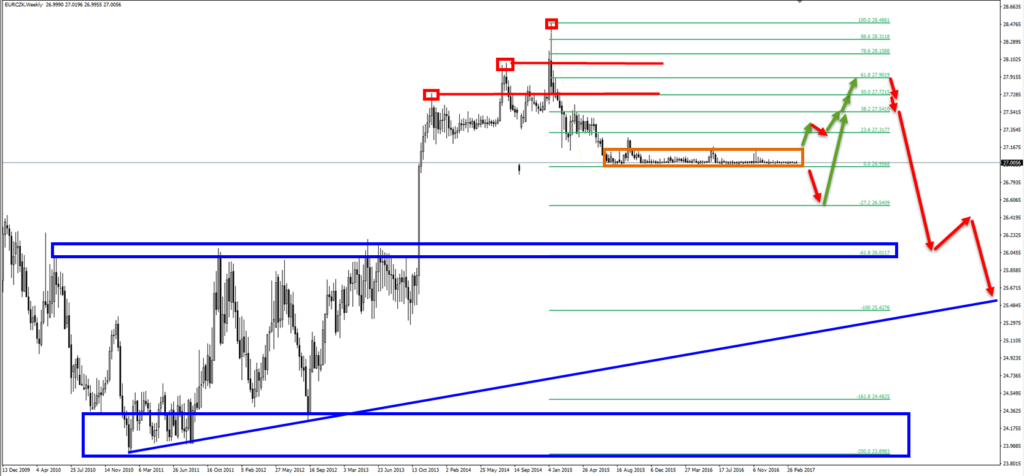

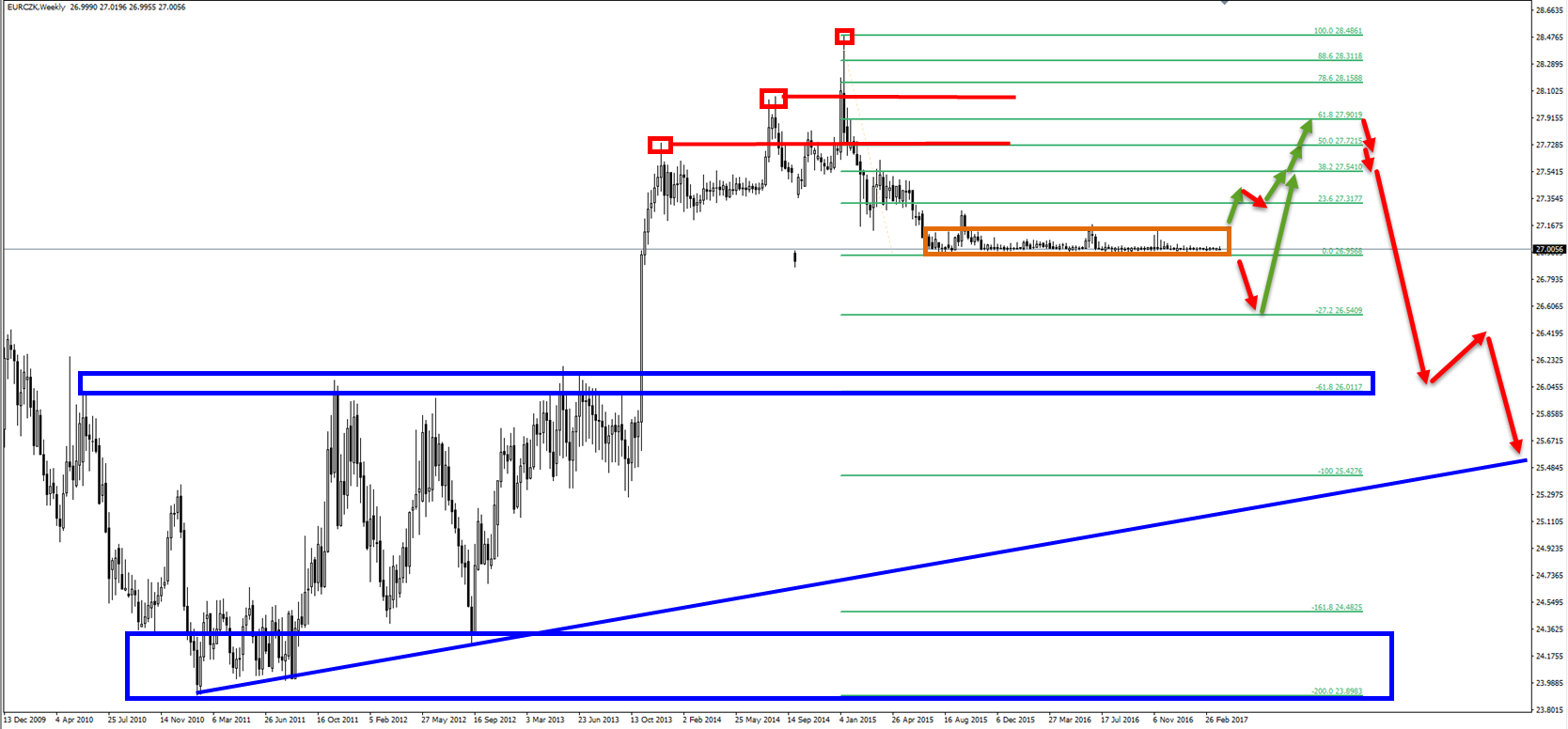

What will happen with the EUR/CZK?

Currently the CNB is committed to intervene unlimitedly on the FX market (if needed) to weaken the Czech Crown (CZK) so that the exchange rate against the Euro is kept at 27. The CNB prevents the appreciation of the CZK by automatic and potentially unlimited interventions, by selling the CZK and buying the foreign currency, the Euro.

Once the CNB removes the intervention, the CNB allows the CZK exchange rate to move freely once again according to the supply and demand of the Forex market. This is very similar to the EUR/CHF peg at 1.20 which was maintained by the Swiss National Bank (SNB).

The problem with interventions from Central Banks is that the release can be very volatile, as was certainly seen with the EUR/CHF which fell from 1.20 to below 0.90. Central banks create an unnatural playing field and trading this environment is a high risk endeavor. Especially because speculation is most likely increasing and the pressure on the CNB to react is mounting.

Personally we are not fans of trading setups that are based on the Central Bank’s decision because they call the shots: when and how the peg is released. We however doubt that the EUR/CZK will move as volatile as the EUR/CHF did when its FX market intervention was released.

Generally speaking it might make sense to consider trading decisions that are not based on leverage, especially high leverage:

- For instance, moving Euro (without leverage) into Czech Crown if you can keep the CZK for 1-2 years should be a profitable move.

- Not exchanging your CZK into Euro but waiting till a few months from now also could make sense.

For those that still want to use a bit of leverage or for those that are looking for the best entry point, let me explain our thoughts about the potential EUR/CZK movement in this video:

Many green pips!

Chris and Nenad

Twitter: @elitecurrensea

Youtube: Elite CurrenSEA

Live webinars at: Admiral Market

Leave a Reply